Current Estimates of State Budget

The state's largest single fund is the General Fund. State collections of individual income taxes, sales taxes, corporate, and other taxes are deposited into this fund. Expenditures from the state General Fund can be made for any authorized state activity. Spending is limited by legislative appropriations. This fund receives the most attention from the Governor and the Legislature and is the fund most referenced when the state has a deficit or surplus.

The table below shows the current estimates for the current biennium for general fund revenue, spending, reserves and budgetary balance as of February 2025 Forecast. For additional detail, go to the current operating budget page.

Other state funds are less flexible. For example, certain revenues such as gasoline taxes or hunting license fees are deposited into funds that can only be spent for the specific purposes established in the state constitution or in state statutes. In budget terms, these are referred to as dedicated funds. For additional information on non-general fund revenue and spending, go to the consolidated fund statement on the current operating budget page.

The Biennial Budget Cycle

Minnesota enacts budgets for a two-year cycle (a biennium), beginning on July 1 of each odd-numbered year. By law, the Governor must propose a biennial budget in January of odd numbered years. Once enacted by the Legislature, the budget can be modified in the "off-year" legislative session. As a result of state forecasts and other changes, it has become common for the Legislature to enact annual revisions to the state's biennial budget. These revisions are referred to as supplemental budgets. The state's constitution requires Minnesota to maintain a balanced budget by the end of the budget cycle.

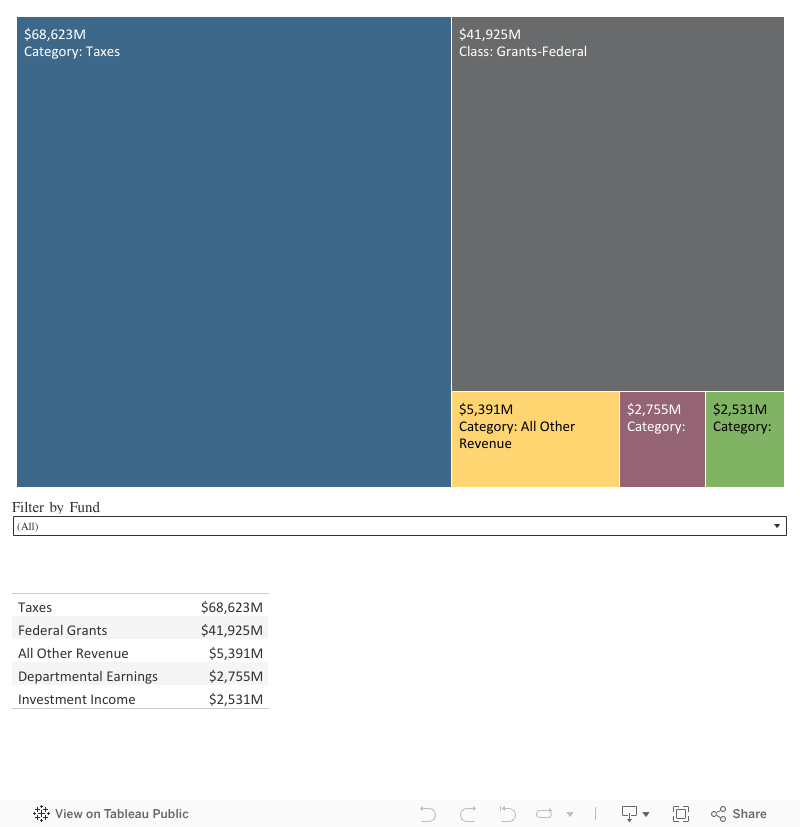

Where the Money Comes From, FY 2024-25 Biennium

Minnesota receives most of its revenue from general taxes, licenses, fees, and federal grants. State laws and statutes designate where each individual revenue source must be deposited and any restrictions on how it should be used to support state operating expenditures. The chart below displays the major revenue sources for all state funds in the current biennium. The Department of Revenue collects most of the general tax revenues, while federal grants, fees and other revenues are collected by various agencies.

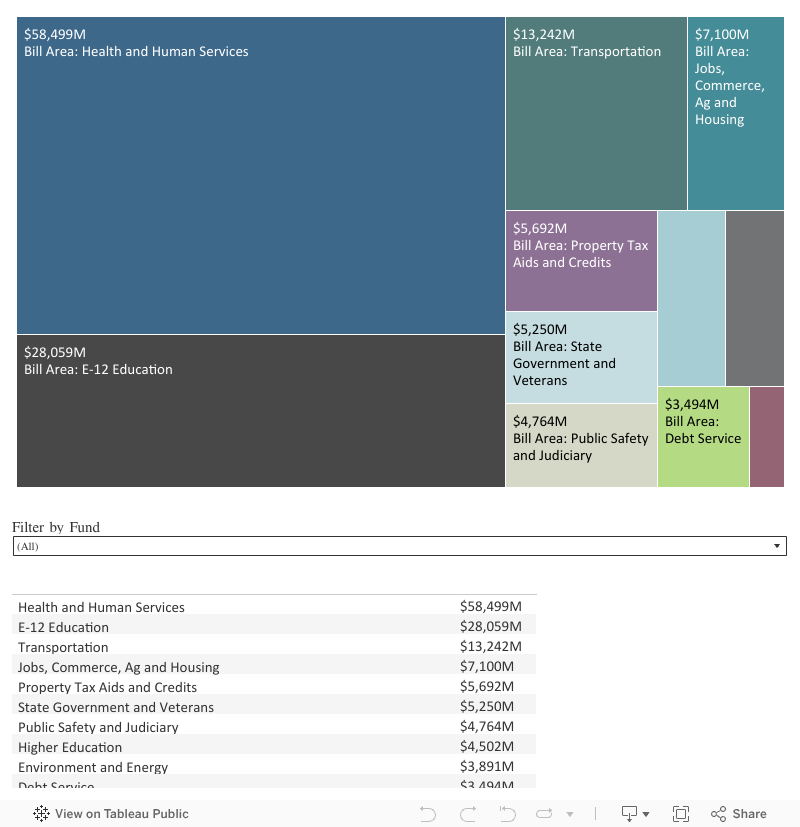

Where the Money is Spent, FY 2024-25 Biennium

Spending in the state budget is allocated to 10 separate “bill areas”

- E-12 Education, state support for pre-kindergarten through grade 12 education

- Higher Education, state funding for public universities, state and community colleges

- Property Tax Aids and Credits, local government aid and grant programs, property tax refunds

- Health and Human Services, funding for mental health and other institutions, public assistance, health care, early childhood, and general public health programs

- Public Safety and Judiciary, includes state courts, correctional institutions, and crime-related programs

- Transportation, transportation systems, highway construction and maintenance, and the Minnesota State Patrol

- Environment, programs for environmental protection and recreation.

- Economic Development, Energy, Agriculture and Housing, programs for improving opportunities, growth, housing stability, agriculture and economic success to individuals, and businesses and communities

- State Government and Veterans, including administrative, constitutional offices, and legislative agencies

- Capital Projects and Grants, payment of principal and interest on state bonds along with other capital project spending

- General Fund Refinance, prior year general fund expenditures that have been refinanced to federal resources

State expenditures are primarily paid for by general state tax revenues, federal funds, fee revenues, and other sources – such as earned interest and lottery receipts. The capital budget is primarily funded through general obligation bonds. Principal and interest on state general obligation bonds is paid by the general fund in the operating budget. The General Fund - State Operating Budget.

Who Receives General Fund Money

As described above, general fund spending is allocated among various functional areas of the budget. But, also the spending occurs in different ways and can be broken down by who gets the money - operating expenditures, grants, and payments to individuals. In FY 2019, 58 percent of general fund payments went to grants like payments to school districts and local governments, while 29 percent were made to, or for the benefit of individuals, such as health care payments, property tax refunds, and student grants. State agency operating expenses accounted for 12 percent of spending.

Budget and Accounting Structure

State government is organized into over 100 agencies, boards, and commissions representing a wide range of services. While many of the largest state agencies report directly to the Governor, elected officials or independent boards manage others. All agencies receive their spending authority from legislative authorizations called 'appropriations' that impose a legal limit on spending. The state's accounting system includes nearly 200 discrete funds that operate much like individual bank accounts with specific sources of revenue.