by Alessia Leibert

March 2025

Prospective college students wrestle with questions like: Which schools close to home have the most appealing programs? Will I be able to find a job after college that allows me to pay back my student loans and support myself and my family?

DEED's new Graduate Earnings and Cost Calculator can help inform these decisions by answering three key questions:

Interactive filters allow users to slice the data by six regions and 567 majors. The tool is a companion to the Graduate Employment Outcomes tool, which provides employment outcomes of graduates by program and institution of higher education in Minnesota.

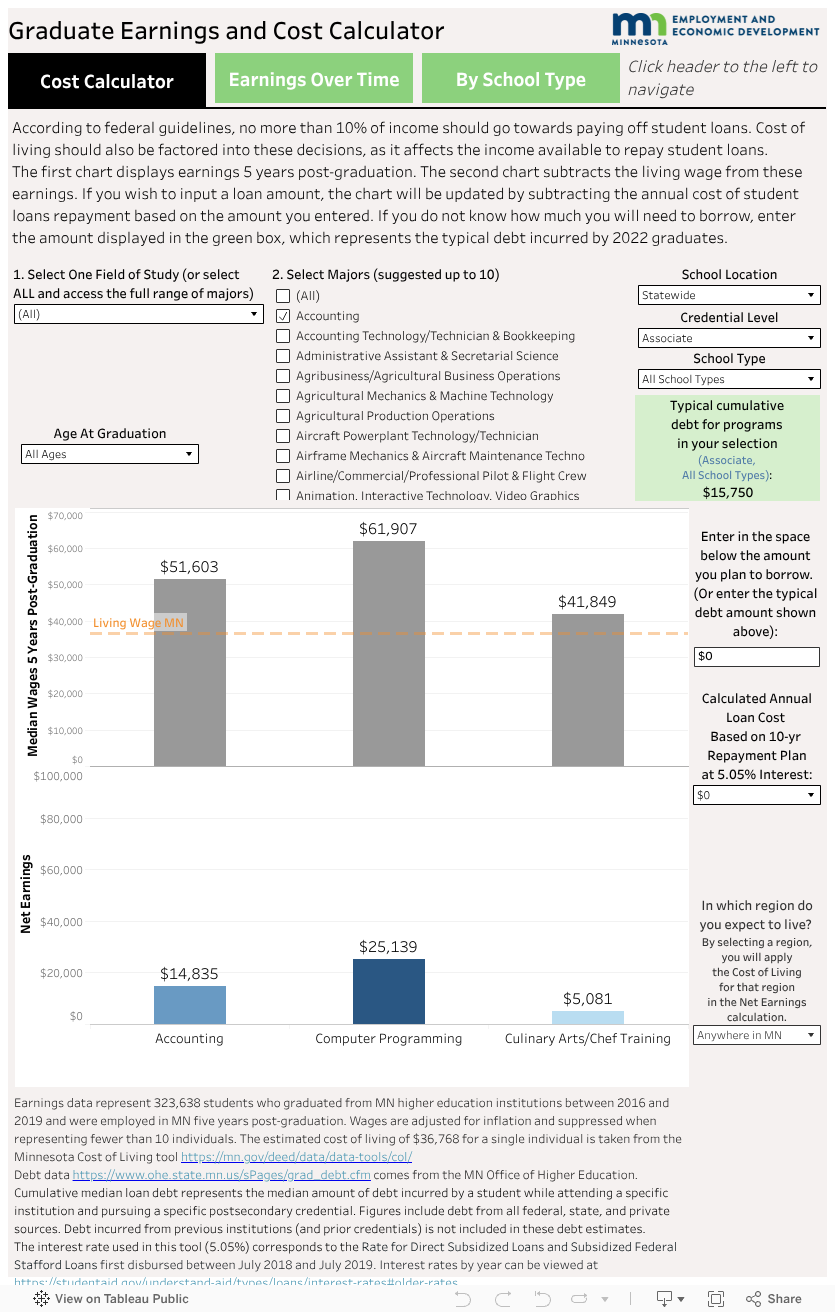

The tool's most unique feature is the Cost Calculator, shown in the first tab (see Figure 1). The calculator helps select a type of school and major based on the comparison between estimated future earnings and estimated costs.

Figure 1

Most schools in Minnesota publish an estimated annual cost of attendance, which typically factors in tuition and fees, living expenses, books and supplies. However, only a minority of students pay the full sticker price. Most college websites feature a Net Price Calculator that estimates the difference between the published price minus any grants, scholarships and education tax benefits for which students may be eligible. This tool calculates estimated costs on the basis of the amount students are planning to borrow.

To illustrate how the calculator works, we selected associate degrees in three majors: Accounting, Computer Programming and Culinary Arts. The upper chart in Figure 1 displays earnings five years post-graduation, while the lower chart subtracts the estimated living wage in Minnesota ($36,768) from these earnings. This is the simplest Net Earnings calculation, which does not take into account borrowing costs.

In the next step we factor in the cost of student loans. To do that, users input the total loan amount in the field shown to the right of the chart. The chart will immediately update by subtracting the annual cost of student loan repayment corresponding to the loan amount entered. This annual cost will dynamically display under "Calculated Annual Loan Cost Based on 10-yr Repayment Plan at 5.05% interest."

Users who do not know how much they will need to borrow can enter the cumulative debt amount displayed on the upper-right of the chart ($15,750) which represents the debt incurred by 2022 graduates in the selected credential (associate degree) and published by the Minnesota Office of Higher Education. We can think of this as the typical amount students borrowed, presumably because they believed other sources of funding (work, scholarships or grants) to be insufficient. Once we enter the number 15,750, the lower chart is refreshed with newly calculated Net Earnings that take into account the annual cost of repaying the loan, assuming an interest rate of 5.05%1 with a 10-year term. Figure 2 displays the results of the calculation.

The vertical bar corresponding to programs in Culinary Arts dropped to $3,071: Expected earnings five years after graduation are barely enough to cover both the estimated cost of living and the estimated cost of the loan for a year. Programs in Accounting and Computer Programming offer a better value overall.

This example does not factor in the type of school at which the program is offered, which influences the typical debt amount. That's where the "School Type" filter comes in handy. If a student expects to complete a Culinary Arts program at a private for-profit college, she can set the filter to "Private For-Profit" to find out the typical cumulative debt for this type of school. The amount is $24,973, translating to a higher cost of servicing the loan than seen in Figure 2. How much higher? After entering the new amount, the annual loan cost changes to $3,186. At that point, the Culinary Arts net earnings become negative and colored in red, implying that earnings are insufficient to cover a conservative estimate of costs. In contrast, if the student were to complete the same program at a Minnesota State 2-Year Institution, the estimated total amount of debt would be $12,459, resulting in positive net earnings.

The Net Earnings formula can be viewed in the tooltip that appears by hovering over the vertical bar corresponding to Culinary Arts in the lower chart. See below.

The calculator demonstrates how certain types of schools can lead to higher salaries, but also to higher debt. Since the cost of education (and, therefore, the typical amount borrowed) increases by credential level, students face a trade-off between the earnings potential of a major and the cost of attendance. When the price of a loan is factored in, more affordable schools may offer a better value even within the same major.

The tool also gives the option of customizing the cost-of-living estimate to a specific region of Minnesota. By selecting a region from the filter, the cost-of-living estimate used in the calculation changes from $36,768 (the default) to the estimate for the region, taken from DEED's Cost of Living tool. A student who completed an associate degree in Culinary Arts and lives in Northeast Minnesota after graduation, where the cost of living is lower than the state as a whole, will have higher net earnings than a student who completed the same program but lives in the Twin Cities Metro.

A filter by age is also available. Students who expect to complete a post-secondary credential before age 26 are encouraged to select the "Younger than 26" option to obtain a more accurate picture of the earnings outcomes they might experience.

In conclusion, the tool allows users to run "what if" scenarios to determine the affordability of various school types and program options.

When exploring the Cost Calculator for programs beyond bachelor, it is important to keep in mind that the cumulative median debt measure used in the calculation captures only the debt incurred to complete the selected credential, not prerequisite credentials. We have to keep this in mind when using the estimates of "Typical Cumulative Debt" corresponding to master's degrees, graduate certificates, doctorates and professional degrees. Figure 3 shows a master's program in Counseling Psychology as an example.

As shown on the upper-right of the chart, the typical loan amount borrowed by students who completed a master's degree in Minnesota is $37,600, which translates to an annual loan cost of $4,797 including interest. This means a borrower who majors in Counseling Psychology will have net earnings of $22,777 a year. But these net earnings do not capture the cost of completing a bachelor's. If a student has already borrowed the typical amount for a bachelor's ($24,736) and enrolls in the master's program before fully repaying the first loan, for that student to borrow another $37,600 is risky.

How can the risk be mitigated? According to federal guidelines, no more than 10% of income should go towards paying off student loans. The borrowing cost of $4,797 shown in Figure 3 for a master's degree in Counseling Psychology represents 7% of median earnings. Since 7% is below the 10% threshold, borrowing this amount to attain this major appears financially sound. It would be risky if there are previous loans to repay.

While an advanced degree can lead to higher lifelong earnings2, the burden of two loans of $24,736 and $37,600 each risks depriving students of a significant portion of disposable income for years.

The following tips/caveats should be kept in mind when using the Cost Calculator:

A key consideration when planning for college is the availability of a program near home and in a type of school students can afford. The tool lets users compare earnings outcomes not only across majors, but also across school types within each region in Minnesota, as shown in Figure 4. By zooming in on two majors (Accounting and Registered Nursing), one award level (bachelor's) and one region (the Twin Cities) we can identify the school type with the best outcomes. We further narrowed down results to the youngest age group, which is generally more representative of the undergraduate student population.

At the bachelor level, these two majors are offered in four types of schools: Minnesota State 4-year schools, private for-profit, private not-for-profit and the University of Minnesota. Graduates from the University of Minnesota attained the highest wages in both majors. Accounting programs (blue bars) offered at Minnesota State 4-year schools led to the lowest annual wages, $68,903. In contrast, Registered Nursing programs (red bars) at Minnesota State 4-year schools earned very high wages.

The findings from Figure 4 can provide a good starting point for prospective students who want to identify affordable schools with a record of graduates' earnings that is comparable to pricier or more selective schools5. This knowledge, in turn, can help determine what programs at what types of schools have the highest value.

Whether a degree is worth it depends on costs (time and money) and returns (potential earnings). The Graduate Earnings and Cost Calculator offers students and families an unprecedented level of detail to figure out this equation.

1The rate of 5.05% corresponds to the rate for Direct Subsidized Loans and Subsidized Federal Stafford Loans, for loans first disbursed between July 1, 2018 and July 1, 2019. These rates apply to undergraduate students. The list of interest rates by year is available. For the most current period (2024-2025), the interest rate for Direct Subsidized Loans and Direct Unsubsidized Loans for undergraduate students is 6.53%, while for graduate or professional students the interest rate for Direct Unsubsidized loans is 8.08%. Source: Federal Student Aid.

2Since master's degree holders typically experience higher wage growth, this net income will likely grow over time. The first tab of the tool shows earnings grows until the 6th year post-graduation to get a sense of what to expect.

3Since earnings do not follow a normal distribution, it is useful to divide their distribution into four parts called quartiles. The tool's tooltip shows the wage corresponding to the start of the second quartile (also called 25th percentile) and the end of the third quartile (75th percentile). If the difference between these to wage figures is very large, and the number of employed students is very low, the median figures could be volatile and should be interpreted with caution.

4Information on the share of graduates employed fulltime year-round is available in the tool's fourth tab by hovering over the horizontal bar. In the specific case of Master's degrees in Counseling Psychology, All Institution Types, All Ages, Statewide, we see that 52.5% of graduates were employed fulltime year-round, implying that the remaining 47.5% were employed part-time or seasonally during the fifth year.

5To explore outcomes by individual school, users can visit the Graduate Employment Outcomes (GEO) tool searching for the CIP program code indicated in the tooltip that appears when hovering over the horizontal bars.